How much car can I afford? sounds simple… until you’re standing at a dealership, keys dangling, salesperson smiling, and suddenly that budget you promised yourself feels flexible. I’ve been there. More than once.

Buying a car is one of the biggest financial decisions most of us make outside of housing. Get it right, and your car is just a helpful tool that gets you places. Get it wrong, and it becomes a monthly stress machine that quietly drains your bank account. This article isn’t here to shame you into buying a 2003 beige sedan (unless that’s your thing). It’s here to help you buy a car you can enjoy and afford without ramen-for-dinner regret.

This article isn’t here to shame you into buying a 2003 beige sedan (unless that’s your thing). It’s here to help you buy a car you can enjoy and afford without ramen-for-dinner regret.

We’ll talk real numbers, real life, and real mistakes. No financial-guru fluff. Just practical advice you can actually use.

The Biggest Lie About Car Affordability

Let’s clear this up right now: If a dealer says you can “afford” it, that only means the bank approved the loan, not that it’s good for your life.

Approval ≠ affordability. Banks look at risk. You should look at comfort. I’ve seen people approved for $60,000 cars while barely saving anything each month. Sure, they made the payment… but everything else suffered.

True affordability means:

- You can make the payment comfortably

- You’re still saving money

- You’re not stressed every time gas prices rise

- Repairs don’t wreck your month

That’s the standard we’re using here.

Step One: Know Your Monthly Comfort Zone

Before prices, before brands, before test drives, you need to know your number.

The Golden Monthly Car Budget Rule

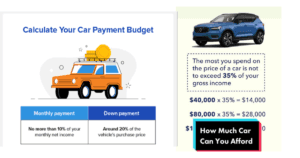

Most financial pros agree: All car costs combined should be 10–15% of your take‑home pay. That includes:

- Car payment

- Insurance

- Gas

- Maintenance

- Registration & fees

Example:

If you take home $4,000/month:

- 10% = $400 (very safe)

- 15% = $600 (upper comfort limit)

If your car costs more than that monthly, something else in your life will pay the price.

Real‑World Monthly Car Cost Breakdown

Here’s where most people mess up: they only think about the payment.

Typical Monthly Costs (U.S. Averages)

| Expense | Economy Car | Mid‑Size Car | Luxury Car |

| Loan Payment | $250–$400 | $450–$650 | $800–$1,200 |

| Insurance | $100–$150 | $150–$220 | $250–$400 |

| Gas | $100–$180 | $120–$220 | $150–$300 |

| Maintenance | $50–$100 | $80–$150 | $150–$300 |

| Total Monthly | $500–$800 | $800–$1,200 | $1,300–$2,200+ |

Seeing it all together hits different, right?

The 20/4/10 Rule (Still Solid, Still Relevant)

This rule is old-school,ol but it works.

The Rule Explained

- 20% down payment

- 4-year loan max (48 months)

- 10% of gross income toward car costs

Why It Works

- You avoid being upside-down on the loan

- You pay less interest

- You keep flexibility in your budget

Is it strict? Yes. Is it smart? Also yes. If you can’t hit this rule, it doesn’t mean you can’t buy a car; it just means you should be extra cautious.

How Much Car Can I Afford Based on Income?

Let’s talk numbers people actually search for.

Safe Car Price Guidelines

| Annual Income | Max Car Price (Smart) | Stretch Price (Risky) |

| $30,000 | $8k–$10k | $12k |

| $40,000 | $12k–$15k | $18k |

| $50,000 | $15k–$20k | $25k |

| $75,000 | $22k–$30k | $38k |

| $100,000 | $30k–$40k | $50k |

| $150,000+ | $40k–$60k | $75k+ |

These assume average debt and expenses. If you have student loans, kids, or high rent, aim lower.

New Car vs Used Car: The Real Cost Difference

New Cars

Pros:

- Warranty

- Latest tech

- No mystery history

Cons:

- Massive depreciation

- Higher insurance

- Higher loan balances

Used Cars

Pros:

- Slower depreciation

- Lower purchase price

- Cheaper insurance

Cons:

- Potential repairs

- Less tech

- Shorter warranty (or none)

My Honest Take

If you’re asking “How much car can I afford?” instead of “Which luxury trim do I want?”, a 2–5 year old used car is almost always the smartest move.

Buyer’s Guide: Choosing the Right Car for Your Budget

1. Be Honest About Your Lifestyle

- Daily commuter?

- Weekend road trips?

- Kids or pets?

- City parking?

Don’t pay for features you won’t use.

2. Prioritize Total Cost of Ownership

Some cars are cheap to buy and expensive to own. Look at:

- Insurance rates

- Reliability history

- Fuel economy

- Maintenance costs

3. Avoid the Loan Trap

Longer loans = lower payments = higher total cost. A 72‑month loan is not a deal. It’s a warning sign.

4. Leave Room for Life

If your car payment prevents:

- Saving

- Traveling

- Emergencies

…it’s too much car.

The Emotional Side of Car Buying (Let’s Be Real)

Cars are emotional purchases. Status, comfort, nostalgia, it’s all real. But here’s the truth I learned the hard way:

The stress of an expensive car lasts longer than the thrill of owning it. A car you can easily afford feels better every single month.

Common Mistakes That Blow Up Budgets

- Focusing only on the monthly payment

- Ignoring insurance costs

- Rolling old debt into a new loan

- Choosing longer loan terms

- Buying based on approval, not comfort

Avoid these, and you’re already ahead.

Read More: Car Spare Parts List

FAQs: How Much Car Can I Afford

How much should I spend on a car monthly?

Ideally, 10–15% of your take‑home pay, including all car expenses.

Is it okay to spend more if I love cars?

Yes, if you’re debt‑free, saving aggressively, and it doesn’t hurt your goals.

Should I buy new if I can afford it?

You can, but used cars usually offer far better value.

How much down payment should I put?

At least 10–20%. More is always better.

Is leasing cheaper?

Lower payments, yes. Cheaper overall? Rarely.

Final Thoughts: The Right Car Is the One That Lets You Sleep at Night

The best answer to “How much car can I afford?” isn’t a number; it’s a feeling. If your car payment:

- Feels manageable

- Doesn’t stress you out

- Still allows saving and living

You did it right. A car should support your life, not control it.